Pandemic and Progress: A Post-COVID Reimagining of the Gulf Cooperation Council (GCC)

The COVID-19 Pandemic has resulted in tragic economic, social, and political consequences around the world. But for GCC countries, the shock is particularly dramatic as the impacts of mitigating economic damage directly associated with COVID-19 are exacerbated by the lowest oil prices in seventeen years. The spread of the virus is likely to reduce global demand for oil while the required containment measures and restrictions continue to affect other economic sectors. The economic impact for 2020 has been significant, and while 2021 projections are optimistic, whether there is a rebound will depend on still-unpredictable exogenous determinants such as global recovery rates, the success of mass vaccination campaigns, and the behavior of international financial markets (Figure 1).

Although the immediate priority of GCC countries is to address the social and economic harm posed by the pandemic, they should also look to capitalize on this opportunity to engage in a comprehensive reform agenda that tackles some of the region’s structural issues. Laying the groundwork for a sustainable recovery and resilient economy should be based on 1) continuing to support public and private-sector digitization; 2) promoting economic diversification by implementing business, labor, and human capital reforms; and 3) increasing efforts to shift towards a more sustainable and inclusive GCC. Although GCC governments have already made substantial progress in implementing certain structural reforms, it is vital that policy makers create a roadmap to reduce dependence on oil and natural gas, bolster migration to digital technologies, and prepare their human capital for the needs of tomorrow. By anticipating future trends in a post-COVID world, the GCC has the potential to not only reshape the direction and speed of future economic recovery, but also help build resilient and sustainable societies.

Keys for Innovation: Reimagining the future of the GCC

1) As a consequence of COVID-19, the rapid migration to digital technologies will continue to accelerate, requiring political leadership to support development and adoption of new capabilities.

Recent studies have shown that in 2020, adoption of digital technologies by consumers and businesses increased at unprecedented rates.[1] Banks have transitioned to remote service teams and launched digital outreach to customers to make flexible payment arrangements for loans and mortgages; grocery stores have shifted to online ordering and delivery as their primary business modality; schools in many locales have pivoted to 100 percent online learning; and healthcare providers have begun delivering telemedicine. This turn toward digital technologies has allowed governments to respond to the COVID-19 crisis in the near-term, mitigate socio-economic issues in the mid-term and reinvent existing policies and tools in the long-term.

In the GCC region, adoption of information and communications technologies (ICT) has remained high — close to that of Advanced Economies — while a strong digital infrastructure (roll-out of 5G technology and expanded fiber networks) has the potential to continue promoting internet-based businesses in the region. Further, financial digital technologies have increased access to financial services among underserved populations and supported inclusive growth, benefiting primarily SMEs. Gross value added in the region’s financial services sectors has expanded at average annual real growth rates of up to 10 percent, and in 2019 contributed between 5 and 16 percent of national GDP within the GCC. Government authorities should capitalize this momentum in digital innovation by making digital transformation a priority by:

A) Fostering new forms of partnership with the private sector. By partnering with the private sector to design and implement well-structured stimulus measures, regulations, and innovation ecosystems, governments can help prepare their citizenry for technology-focused futures and improve the long-term competitiveness and resilience of strategic industries.

B) Increase public-sector productivity. The COVID-19 crisis has required public servants to improvise and provide rapid solutions to various logistic, administrative, and operational challenges. Optimizing government services with the help of automation and digital technologies can strengthen public service productivity.

C) Ensure faster, better decision making that harnesses data and analytics. COVID-19 has presented new ways to harness, use, and apply data and analytics to inform policy and decision making. Governments should foster the strategic use of technologies and information to improve governance by increasing transparency and citizen collaboration.

The accelerated use of the internet and related ICT by governments provides a promising approach to organise tasks, routines, and internal processes, as well as a low-cost and convenient medium to interact with citizens. GCC countries should focus on supporting this digital revolution and leveraging this opportunity to bolster real private sector development.

2) The twin impacts of COVID-19 and muted oil prices have demonstrated the importance of diversifying GCC economies.

Given that continuing to expand government employment is inconsistent with the GCC’s fiscal projections, a strong private sector will be vital to get on the path to economic recovery and absorb future labor. The post-COVID-19 GCC will require redoubled efforts to support growth-oriented, export-driven sectors that are not dependent on revenues from oil and gas.

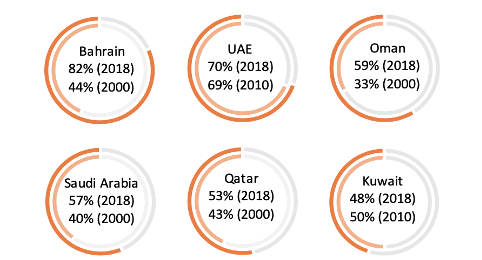

Over the past 20 years, all GCC countries have seen a shift in their GDP composition in favor of non-oil sector expansion and growth (Figure 3). However, rates have varied by country: by the end of 2018, for example, Bahrain and the UAE had the most diversified economies in the region, while Kuwait and Qatar remained the most oil-dependent. A large part of GCC diversification programs have been associated with progressive regulatory reforms to their business environments. Between 2018 and 2019, Bahrain, Kuwait, and Saudi Arabia ranked among the top 10 global improvers in the World Bank’s Doing Business Indicators, evidencing their commitment to business-facilitating reforms. Further, all GCC countries have implemented reforms designed to facilitate trade and attract foreign investment and expatriate workers. For instance, Abu Dhabi introduced a law regulating public-private partnerships (PPPs) to encourage private sector participation in technology, urban infrastructure, education, healthcare, housing, and transportation. Saudi Arabia and UAE enhanced their expatriate residency permits, and regional governments are also implementing financial-sector reforms to improve capital adequacy of commercial banks.[2]

Despite the significant progress GCC countries have made, several outstanding issues remain to be addressed to promote an impactful economic diversification:

A) Continuing to support a GCC-wide internal market would benefit private sector growth, increase the global competitiveness of GCC economies, and contribute to collective diversification efforts. Despite the low trade barriers under the GCC Customs Union Agreement signed in 2003, intra-GCC non- oil trade remains low, at around 10 percent of total non-oil trade.[3] After surging in the early 2000s, FDI inflows into GCC countries have stalled, remaining on average around 1.5 percent of regional GDP despite goals of diversification previously announced.

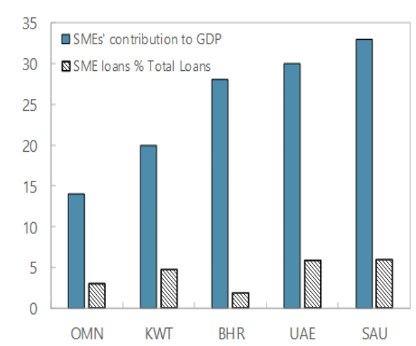

B) Supporting SME development is vital for diversification and genuine private sector growth. Despite representing a substantial part of GCC economies, SMEs face limited access to finance and SME share of total loans is much lower than its contribution to GDP in the GCC (Figure 4). Further, much private sector activity in GCC countries remains linked directly or indirectly to government contracts and spending that, in turn, are funded through revenues from oil and gas. This tends to benefit already established and connected public enterprises and private companies at the expense of more competitive firms. GCC states must focus their efforts on reducing burdensome laws and regulations, allocating a minimum share of government contracts to SMEs, ensuring their access to finance and timely government payments.

3) In the context of an overburdened public sector, a labor reform will be necessary to support non-oil, private sector development and absorb new workers in the coming years. Depending on participation rates, the labor force could grow by an additional 2.5 million GCC nationals by 2025.[4] This offers a huge opportunity to benefit from a growing and increasingly well-educated labor force, but will need to be accompanied by measures to strengthen the private sector employment of nationals.

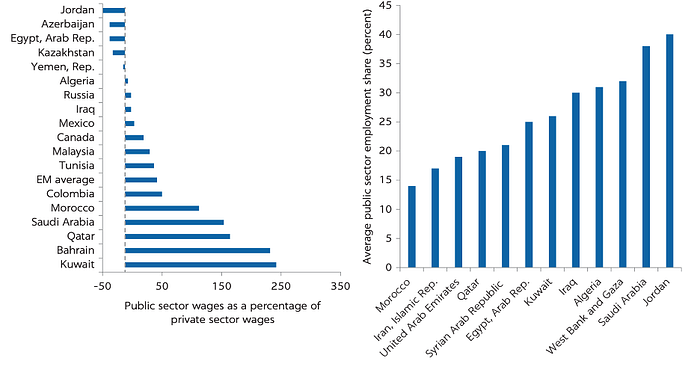

With more generous wages and a virtual guarantee of government jobs, the public sector tends to be much more attractive for nationals than private sector employment. Public sector wages are between 180 percent and 250 percent of private sector wages in Saudi Arabia, Qatar, Bahrain, and Kuwait (Figure 5 left). This wage disparity has led to nationals queueing for public sector jobs; in Saudi Arabia, for example, about 35 percent of total employment is in the public sector, in Kuwait, more than 25 percent, and in Qatar and the United Arab Emirates, about 20 percent ( Figure 5 right). This contrasts with OECD averages, where public sector employment as a share of total employment is about 18 percent.[5] Meanwhile, the liberal entry of foreigners into private sector jobs, which include regulating entry into the country, exit, residency, and work permits for noncitizens means that foreigners perform 75 percent of all jobs in the private sector. This is especially concerning because in the face of the adverse external and fiscal balances that will likely carry over well after the pandemic, an economic diversification program should focus on the creation of private sector jobs and reduction of public expenditures.

A) The COVID-19 pandemic could serve as a “reset button”, catalyzing the political support needed to reformulate labor markets and remove labor-market distortions that break the link between performance and reward. While attempts to bring public sector wages and benefits into alignment with those in the private sector have not been successful, income tax reforms should be explored as a short-term policy that could both increase transparency in wage expectations and better link wages for nationals to productivity and performance. Nevertheless, in order to affect a successful and comprehensive employment reform, GCC will also need to address human capital constraints to prepare the next generation of workers.

4) Expanding human capital will be an inevitable requirement for the long-term sustainability of a diversified, knowledge-based, and private sector–driven economic growth model. Strengthening education systems is key to ensuring GCC nationals have the skills in demand in the private sector and to support diversification efforts. While COVID-19 will likely have many effects on the future of education, it is highly likely that EdTech will play a pivotal role. Given GCC’s already successful efforts in connectivity, large-scale, national efforts should seek to adapt and strengthen remote learning, distance education and online learning to local needs. This rapid evolution in learning methods and channels should be capitalized to mitigate current shortcomings in the educational system.

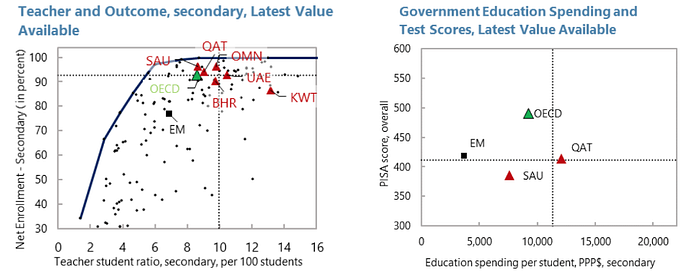

While school enrollment rates in the GCC are broadly comparable to advanced country levels, standardized international test scores indicate significant room for improving the quality of education in the region (Figure 6). When adjusted for the quality of education that children receive, the effective educational attainment in the GCC countries is far lower than in other advanced countries, evidencing a mismatch between education and the labor market. Public school instruction in the six countries tends to emphasize over memorization over critical thinking and other twenty-first-century skills, such as problem solving, collaborative teamwork, and socioemotional and digital skills.

A) Investing in high-quality early childhood development. Investing in the early years of development would allow the GCC countries to improve the lifelong productivity of their people. Studies have shown that a greater return on learning outcomes and lifelong productivity can be achieved when investments are made in the first six years of a child’s development.[6]

B) Preparing youth for the future. Improving learning outcomes and directly responding to labor market needs with the appropriate curricula will be vital in preparing youth for the future after the pandemic.

Aside from enabling a better environment for human capital formation, ensuring environmental sustainability and ecosystems resilience are key for continued economic growth, development, and the quality of life of future generations in the GCC.

5) Diversifying the GCC economies towards more environmentally friendly sectors will be vital to both reduce green-house gas emissions and hedge against the risk and costs involved in the decarbonization of global production. Intensifying regulatory controls on emissions, growing demand for goods and services that consider their environmental footprint, and the advent of low-carbon pose a long-term threat to GCC, hydrocarbon dominated economic models. Applying an integrated approach to stabilization and recovery investments in the aftermath of the pandemic can allow governments to advance their sustainability agenda by integrating the 17 UN Sustainable Development Goals (SDGs) into their national development plans. Across the region, investments in renewable energy are helping meet rising domestic power demand while promoting environmental sustainability and gradually attenuating dependence on the oil sector. Future steps in this direction will be necessary to respond to increasing pressure for adopting sustainable development policies.

A) Beyond diversifying products and exports, a broader approach should focus on diversifying the composition of national wealth. That is, human capital, produced assets, net foreign assets, and renewable natural assets. A broader base of productive assets allows greater flexibility and complexity of products and capabilities, including innovative, new ones that are further away from inherited comparative advantage. Further, climate cooperation can also increase financial flows, accelerate technology transfer and expand the international market access for the GCC firms engaged in knowledge-intensive, environmentally sustainable activities. GCC countries could become business leaders in the technological transition across the MENA and Africa region by providing investments in solar energy, desalination, and global carbon capturing storage technologies for other large emitters. As considerations for sustainability become progressively more important, regional integration and a clear and shared strategy will be fundamental to focus diversification strategies towards more environmentally sustainable economic activities.

[1] International Monetary Fund, Gulf Cooperation council. Economic Prospects and Policy Challenges for the GCC Countries. December 10, 2020.

[2] Ollero, Antonio M., et al. “Economic Diversification for a Sustainable and Resilient GCC (English). Gulf Economic Update; no. 5. Washington, DC: World Bank Group.” (2019).

[3] Baig, Aamer, et al. “The COVID-19 recovery will be digital: A plan for the first 90 days.” McKinsey Digital (2020).

[4] El-Saharty, Sameh, et al. Fostering Human Capital in the Gulf Cooperation Council Countries. The World Bank, 2020.

[5] Kabbani Nader & Mimoune Ben Nejia. Economic Diversification in the Gulf: Time to redouble the efforts (2021).

[6] El-Saharty, Sameh, et al. Fostering Human Capital in the Gulf Cooperation Council Countries. The World Bank, 2020.